Lesson dt 9/9

Scenario 3 –

The price of Gold stays the same

If on 9th Dec 2020, the price is

the same as on 9th sept

2020 then neither ABC nor XYZ would benefit from the agreement.

Possible scenarios in

one graph

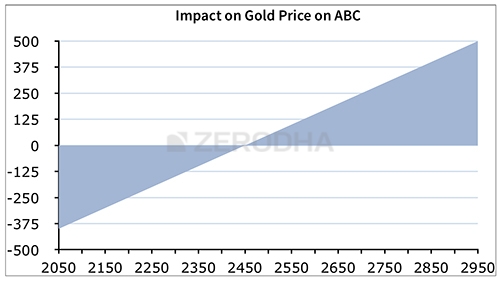

Here is a visual representation of the impact of gold prices

on ABC Jewelers –

As

you can see from the chart above, at Rs.2450/- per gram, there is no financial

impact for ABC. However, as per the graph above we can notice that ABC Jewller’s

financials are significantly impacted by a directional movement in the gold

prices. Higher the price of gold (above Rs.2450/-), higher is ABC JEWLLER’S s

savings or the potential profit. Likewise, as and when the gold price lowers

(below Rs.2450/-), ABC JEWELER’S is obligated to buy gold at a higher rate from

XYZ, thereby incurring a loss.

Similar

observations can be made with XYZ –

At

Rs.2450/- per gram, there is no financial impact on XYZ. However as per the

graph above, XYZ’s financials are significantly impacted by a directional

movement in the gold prices. As and when the price of gold increases (above

Rs.2450/-), XYZ is forced to sell gold at a lower rate, thereby incurring a

loss. However, as and when the price of gold decreases (below Rs.2450/-) XYZ

would enjoy the benefit of selling gold at a higher rate, at a time when gold

is available at a lower rate in the market thereby making a profit

A

quick note on settlement

Assume

that on 9th DEC 2020, the price of Gold is Rs.2700/- per gram.

Clearly as we have just understood, at Rs.2700/- per gram ABC Jewelers stands

to benefit from the agreement. At the time of the agreement (9th SEPT

2020) 15 Kgs gold was worth Rs. 3.67Crs, however as on 9th DEC

2020 15 kgs Gold is valued at Rs.4.05 Crs. Assuming at the end of 3

months i.e 9th DEC 2020, both the parties honor the contract,

here are two options available to them for settling the agreement –

1. Physical

Settlement – – The full purchase price is

paid by the buyer of a forward contract and the actual asset is delivered by

the seller. XYZ buys 15 Kgs of gold from the open market by paying Rs.4.05Crs

and would deliver the same to ABC on the receipt of Rs.3.67 Crs. This is called

physical settlement

2. Cash

Settlement – In a cash settlement there

is no actual delivery or receipt of a security. In cash settlement, the buyer

and the seller will simply exchange the cash difference. As per the agreement,

XYZ is obligated to sell Gold at Rs.2450/- per gram to ABC. In other words, ABC

pays Rs.3.67 Crs in return for the 15 Kgs of Gold which is worth Rs.4.05Cr in

the open market. However, instead of making this transaction i.e ABC paying

Rs.3.67 Crs in return for the gold worth Rs.4.05Crs, the two parties can agree

to exchange only the cash differential. In this case it would be

Rs.4.05 Crs – Rs.3.67 Crs = Rs.38 Lakhs. Hence XYZ would just pay Rs.38 lakhs

to ABC and settle the deal. This is called a cash settlement

We

will understand a lot more about settlement at a much later stage, but at this

stage you need to be aware that there are basically two basic types of

settlement options available in a Forwards Contract – physical and cash.

What

about the risk?

While

we are clear about the structure (terms and conditions) of the agreement and the

impact of the price variation on either party, what about the risk involved? Do

note, the risk is not just with price movements, there are other major

drawbacks in a forward contract and they are–

1. Liquidity

Risk – In our example we have conveniently assumed that,

ABC with a certain view on gold finds a party XYZ who has an exact opposite

view. Hence they easily strike a deal. In the real world, this is not so easy.

In a real life situation, the parties would approach an investment bank and

discuss their intention. The investment bank would scout the market to find a

party who has an opposite view. Of course, the investment bank does this for a

fee.

2. Default

Risk/ / Counter party risk – Consider this, assume the gold

prices have reached Rs.2700/- at the end of 3 months. ABC would feel proud

about the financial decision they had taken 3 months ago. They are expecting

XYZ to pay up. But what if XYZ defaults?

3. Regulatory

Risk – The Forwards contract agreement is

executed by a mutual consent of the parties involved and there is no regulatory

authority governing the agreement. In the absence of a regulatory authority, a

sense of lawlessness creeps in, which in turn increases the incentive to

default

4. Rigidity

– Both ABC and XZY entered into this

agreement on 9th Dec 2020 with a certain view on gold. However

what would happen if their view would strongly change when they are half way

through the agreement? The rigidity of the forward agreement is such that, they

cannot foreclose the agreement half way through.

The

forward contracts have a few disadvantages and hence future contracts were

designed to reduce the risks of the forward agreements.

In

India, the Futures Market is a part of a highly vibrant Financial Derivatives

Market. During the course of this module we will learn more about the Futures

and methods to efficiently trade this instrument!

No comments:

Post a Comment